Where Last Week's Selloff Pain Was Most Acute?

While 2014 has not quite panned out (so far) as the traveling-strategist-roadshow would have hoped, the last few days have been outright perilous for the record high numbers with bullish sentiment sucked into a world of central-bank-suppressed volatility and jawboned utopia. The following charts show where the pain has been(e.g. Greece, Spain, Argentina, European banks) and where it has not been (e.g. gold miners, China, Philipinnes, and Egypt) with the US indices sitting squarely in the middle with some of their biggest losses in months. For now, the BTFATH'ers are absent - even though the drooling mouths of asset-gatherers are demanding the 'cash on the sidelines' use this 2-3-4% drop from the all-time highs to load the boat for retirement heaven... However, some have increasing concerns...

The last 5 days...

But the names change notably for the year so far...

And as a bonus chart (h/t @M_McDonough) here is an interactive chart with the entire dataset described...

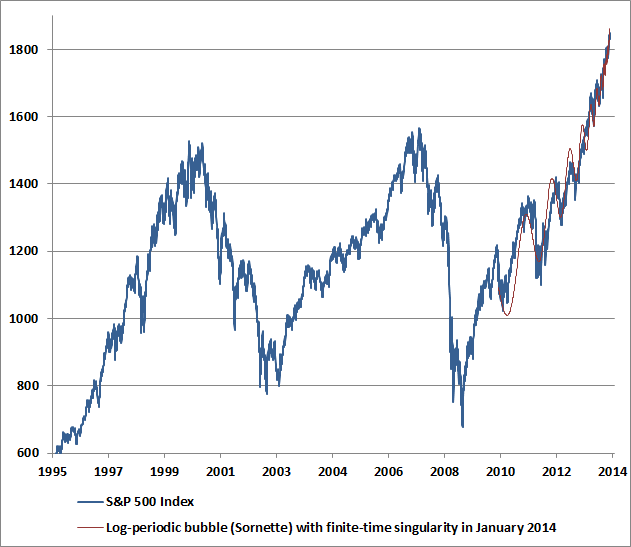

As John Hussman notes - Increasing Concerns and Systemic Instability

...Increasing our concern is also a very well-defined log-periodic bubble running from 2010 to the beginning of this year, which we estimate is now past its “finite-time singularity” (see A Textbook Pre-Crash Bubble).Increasing our concern is the shift to increased short-interval volatility just at the point of that singularity (which we estimate as January 13 – when 2-10 minute fluctuations began looking like the p-wave on a seismogram). Increasing our concern is the highest level of option “skewness” in history as option prices reflect extreme "tail risk" as they did prior to the 1987 crash (the 30-day average of skewness reached a record high on Friday - see Estimating the Risk of a Market Crash).Increasing our concern is a 10-week average of advisory bulls at 57.7% versus just 14.8% bears – the most lopsided bullish sentiment in decades. Add the record pace of speculation on borrowed money, with NYSE margin debt now at 2.5% of GDP – an amount equivalent to 26% of all commercial and industrial loans in the U.S. banking system.Add the currency collapses in Argentina and Venezuela, as well as fresh credit strains and industrial shortfall in China, and one has any number of factors that could be viewed in hindsight as a “catalyst” (as the German trade gap was viewed after the 1987 crash, in the absence of other observable triggers).Against all of these concerns is the recognition that the market doesn’t move in a straight line, and that the risks that concern us here have concerned us – though at less extreme levels – too long for many investors to give them much immediate credibility. Immediacy wasn’t really our strong suit in 2000 or 2007 either, but by the time our concerns played out, we still found ourselves far ahead over the complete cycle, with far less pain than speculators endured. Despite the challenges of an unusual but also unfinished half-cycle, and despite our awkward stress-testing transition, I'm comfortable that the tools we've developed and the benefits of discipline will be evident enough over the completion of this cycle and throughout future ones. But as Kierkegaard wrote, “patience is necessary, and one cannot reap immediately where one has sown.”

Keine Kommentare:

Kommentar veröffentlichen