“Madmen in authority, who hear voices in the air,” Keynes wrote at the end of theGeneral Theory, “are distilling their frenzy from some academic scribbler of a few years back.”

In Argentina, the scribblers are sovereign bond contract draughtsmen.

Proceeding to a global resolution would create an unacceptable risk that Exchange Bondholders could successfully argue that the RUFO clause had been triggered. Although difficult to quantify, this risk clearly exists as there is no precedent on the issue and, as this litigation demonstrates, novel interpretations can be applied to seldom-litigated sovereign debt contract provisions (even where the United States Government takes a contrary position). Moreover, the risk applies not only to an adverse U.S. court ruling, but to the other jurisdictions under which Exchange Bonds were issued, including England and Japan.

Nor can the Argentine public officials who would be involved in such a transaction risk triggering the RUFO clause, as they would face exposure to numerous sources of domestic liability, including criminal charges… Under Argentine law, if public servants cause foreseeable harm to State property, due to either their recklessness or lack of due care, they are subject to impeachment as well as civil and criminal liability…Here, public officials would plainly be exposed to such liability if, notwithstanding the above-mentioned risks of triggering the RUFO clause, they nonetheless took actions that did so and thereby significantly increased the Republic’s liabilities and jeopardized its debt restructuring. This risk of liability on Argentine civil servants is not theoretical; former officials involved in the Republic’s 2001 “megaswap” are still facing recently re-opened investigations in Argentina thirteen years later.

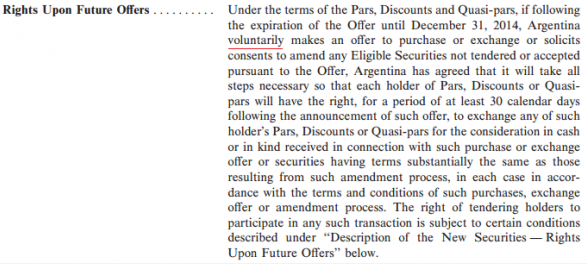

That’s Argentina’s lawyers, writing to Judge Griesa on Monday about the Rights Upon Future Offers clause in its restructured bonds as an obstacle to settling with Elliott and the holdouts. (There’s a hearing later on Tuesday.)

Argentina has previously claimed RUFO activation would bring $120bn of claims, several times its own estimate of maximum holdout liabilities, not a few times the size of its FX reserves. But this is the first time it’s tried to argue that its government officials would actually face a Buenos Aires slammer if they did the wrong thing on RUFO.

What’s so wrong about RUFO then?

The clause allows bondholders who’ve swallowed restructuring terms to demand a piece of the action if Argentina “voluntarily” offers holdouts a better deal within ten years. That is, before the end of this year.

So, in theory, RUFO is a doomsday weapon for enforcing equal treatment between creditors, like the one that holdouts crafted out of their forgotten piece of scribbling — the pari passu clause in defaulted 1994 bonds, whose 68 words have had such effect.

RUFO isn’t a big problem

In theory. In reality, we’ve argued, the RUFO language has loopholes such that it’s unlikely to be a major threat to Argentina when it settles with the holdouts.

When it eventually does that, it sure won’t be “voluntarily” — and if the Republic would like Judge Griesa to confirm this point in writing for the benefit of future litigant creditors, he would probably be rather happy to oblige. Even “settlement” itself could be semantically excluded from the RUFO provision anyway.

And then there would be the forbidding practicalities of a restructured bondholder attempting to sue Argentina over RUFO to obtain a few cents on the dollar more than where the debt now trades in the market after the recent rally… years of litigation possibly, holding illiquid securities. The litigation may in any case have to be led by Bank of New York Mellon, the restructured bonds’ trustee, who as it turns out (full story later in the saga) may be a bit of a wimp about taking legal risks.

And then there would be Argentina’s ability, if it was still worried, to nullify the RUFO clause anyway by asking restructured bondholders to approve amending their contract. Consent (75 per cent of creditors overall) could be forthcoming fairly quickly, if it’s the only obstacle left to a quiet, holdout-free life. In Monday’s filing, Argentina acknowledges that it may, actually, seek consent. Though it insists this “could take months to complete”.

But even then there would be the option of negotiating with holdouts to specially construct the settlement so that it would never trigger the RUFO clause. One design that’s been widely discussed (just not around the negotiating table) is to give the holdouts bonds which would not settle until after the last day of 2014, for example.

And if you still don’t believe all of that, ask some of the angriest restructured creditors out there — the Euro Bondholders owning English-law debt, who have little love for holdouts’ use of the pari passu injunction to block payments on their bonds:

The Euro Bondholders strongly support a negotiated resolution of this case. Although it is unclear whether the Rights Upon Future Offers (“RUFO”) clause would apply to such a resolution, Argentina has raised its potential application as an impediment to settlement… If the RUFO clause is a bona fide impediment to a negotiated settlement of this matter, the Euro Bondholders would be willing to waive the RUFO clause under appropriate circumstances.

The Euro Bondholders even suggest Judge Griesa clarify that Euroclear and Clearstream are allowed to build a list of restructured creditors to contact about a waiver.

Argentina actually doesn’t want the clarification, because it thinks that it has always been allowed to talk to its bondholders anyway. Even though it has suggested that talking to them about waiving the RUFO would be very difficult. Weird.

The paranoid style in sovereign bond contract

In short, Argentina may have plenty of legal manoeuvre here. And yet — as the excerpt above shows — it is apparently obsessed with the tail risk of RUFO activation regardless, to the point of claiming that reckless sovereign restructuring may put its officials in jail. (Given the consequences that usually ensue, might issuing government debt in the first place be a reckless act for Argentine politicians?)

This may of course just be a put-on. Argentina is scrabbling for its last piece oflitigotiation leverage over a settlement with holdouts.

Then again, maybe there is a sense of once bitten, twice shy here. Argentina survived years of legal knife-fights with Elliott, and others, as holdouts attempted to enforce judgments on defaulted bonds against it. What caught the Republic out in the end was a pari passu clause employed by plenty of other bond issuers. A piece of dusty boilerplate. Pari passu had been used against sovereigns before, but never in the US, nor with such wide sweep beyond those mere 68 words. Argentina partly dug its own hole here by passing a Lock Law subordinating holdouts — ironically to limitperceived weaknesses in the RUFO clause. But US courts also looked at wider ‘recalcitrant’ behaviour, a test which may be hard to predict in future.

Perhaps other sovereigns and the market will react to this with sanguinity (altering pari passu clauses, or making sure restructuring is friendlier in the first place). But perhaps the uncertainty that some other dull contractual term may go haywire (negative pledge?) will go on.

Although there may also be some self-awareness here. The reason restructured creditors demanded rights upon future offers in the first place was because they couldn’t trust Argentina (which is why a trustee was appointed as well, and why the Lock Law emerged). By fearing that they may sue for RUFO now –an act contrary to their economic self-interest — perhaps Argentina is showing how untrustworthy it’s been.

Keine Kommentare:

Kommentar veröffentlichen